Orbis — Split Bill

A strategy-led feature design for a Nigerian social pay app — built to convert the habit of splitting money in WhatsApp, not manufacture a new one.

Problem: Splitting a bill is easy. Getting everyone to actually settle up is the part that breaks — and most apps track the split instead of solving the settlement.

Core decision: Design recipient-first, and meet people where money already moves: the chat. Send, pay, confirm — the shortest path to a settled debt.

Outcome: A strategy-led feature design grounded in real Nigerian payment behaviour, built to convert the 40M+ people already splitting money in WhatsApp.

The problem.

Bill-splitting apps are good at arithmetic and bad at outcomes. They tell you who owes what, then leave the hardest part — actually collecting — to awkward reminders in a group chat. The root friction was never the split. It was the settlement gap: the distance between "you owe ₦4,500" and the money landing in someone's account.

And the behaviour is already happening off-platform. Millions of Nigerians split bills inside WhatsApp every day, then chase each other manually. Any product that ignores that reality is asking people to leave the place the money conversation already lives.

If people already split money in their chats, why should they have to learn a new app to finish the job?

Market context.

140M smartphone users in Nigeria, with roughly 60% digital payment adoption — the rails are in place.

40M+ monthly WhatsApp users — where bill-splitting conversations already happen.

Urban professionals, 18–34 as the primary target: high social-spend frequency, high chat usage. Nigerian payment infrastructure is fast and reliable — so the design assumes confidence, not payment anxiety.

Guiding tenets.

Recipient-first. Design for the person who needs to get paid back, not just the person doing the maths.

Meet money where it already moves.The chat is the channel. Don't drag people out of it to settle up.

Minimal friction: send, pay, confirm.Three steps from request to settled. Every extra tap is someone who doesn't pay.

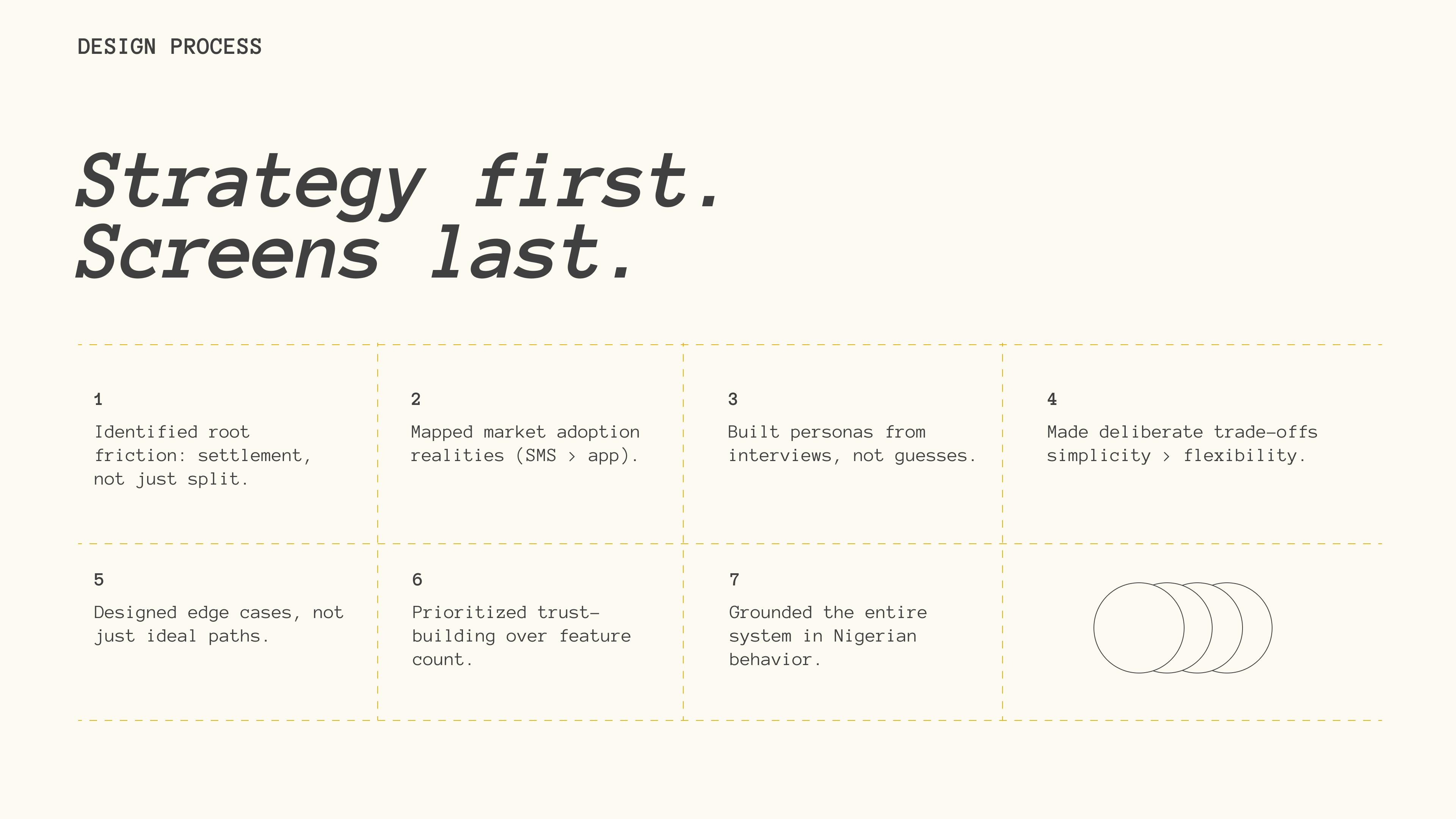

Strategy first. Screens last.

Research and framing before UI — root friction, adoption realities, personas from interviews, deliberate trade-offs, and edge cases grounded in how Nigerians actually split and settle money.

Key design decisions.

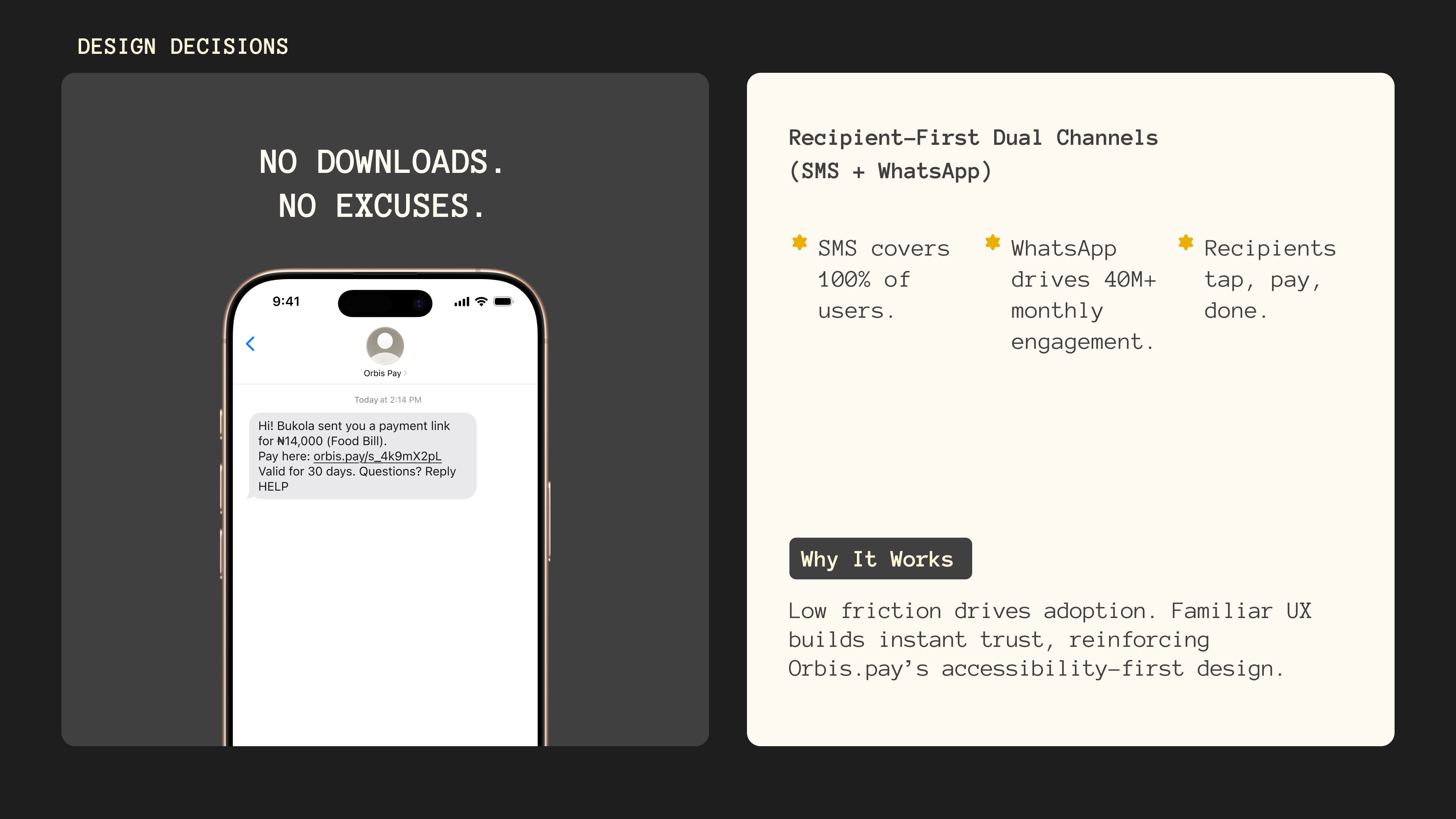

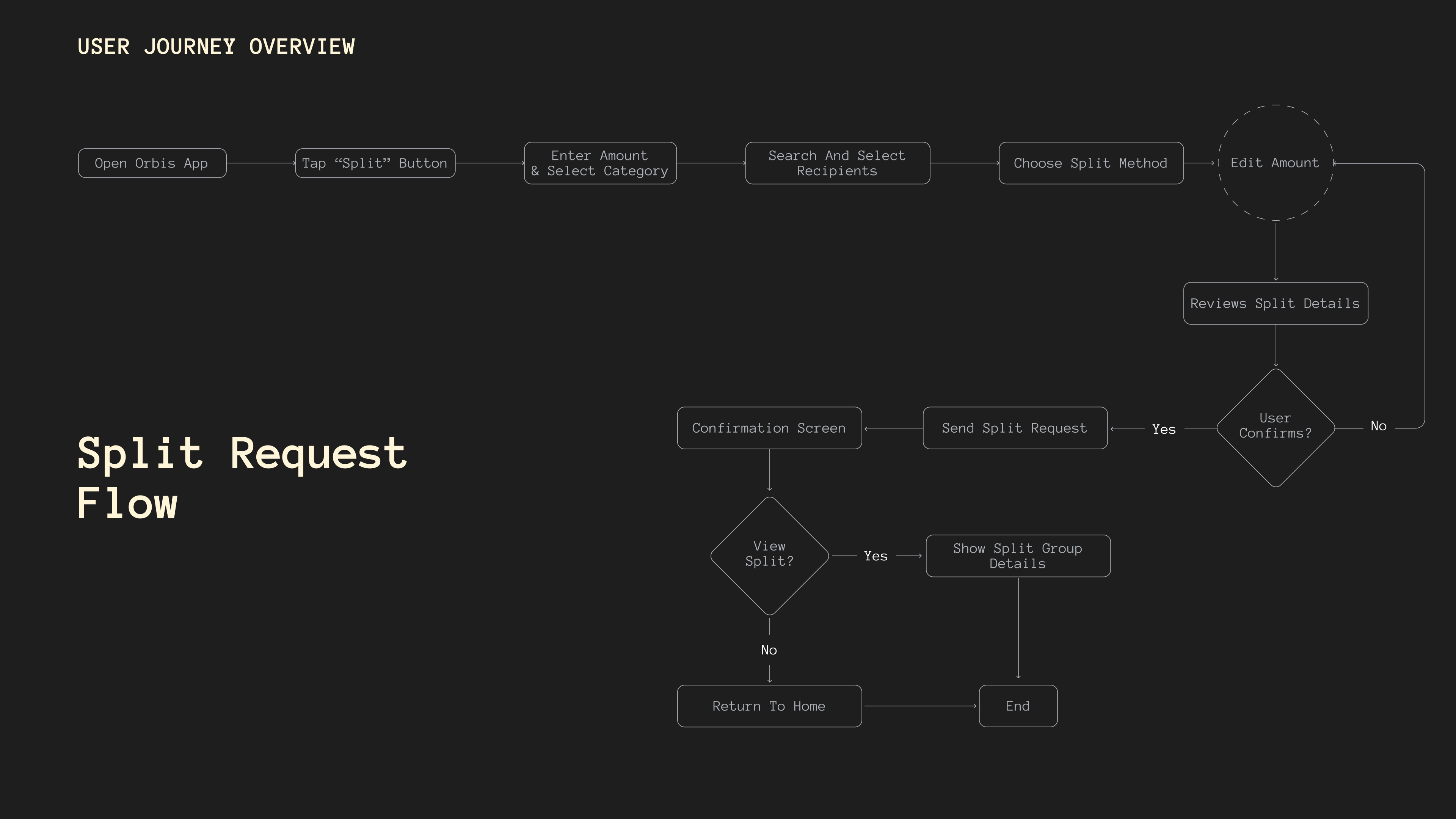

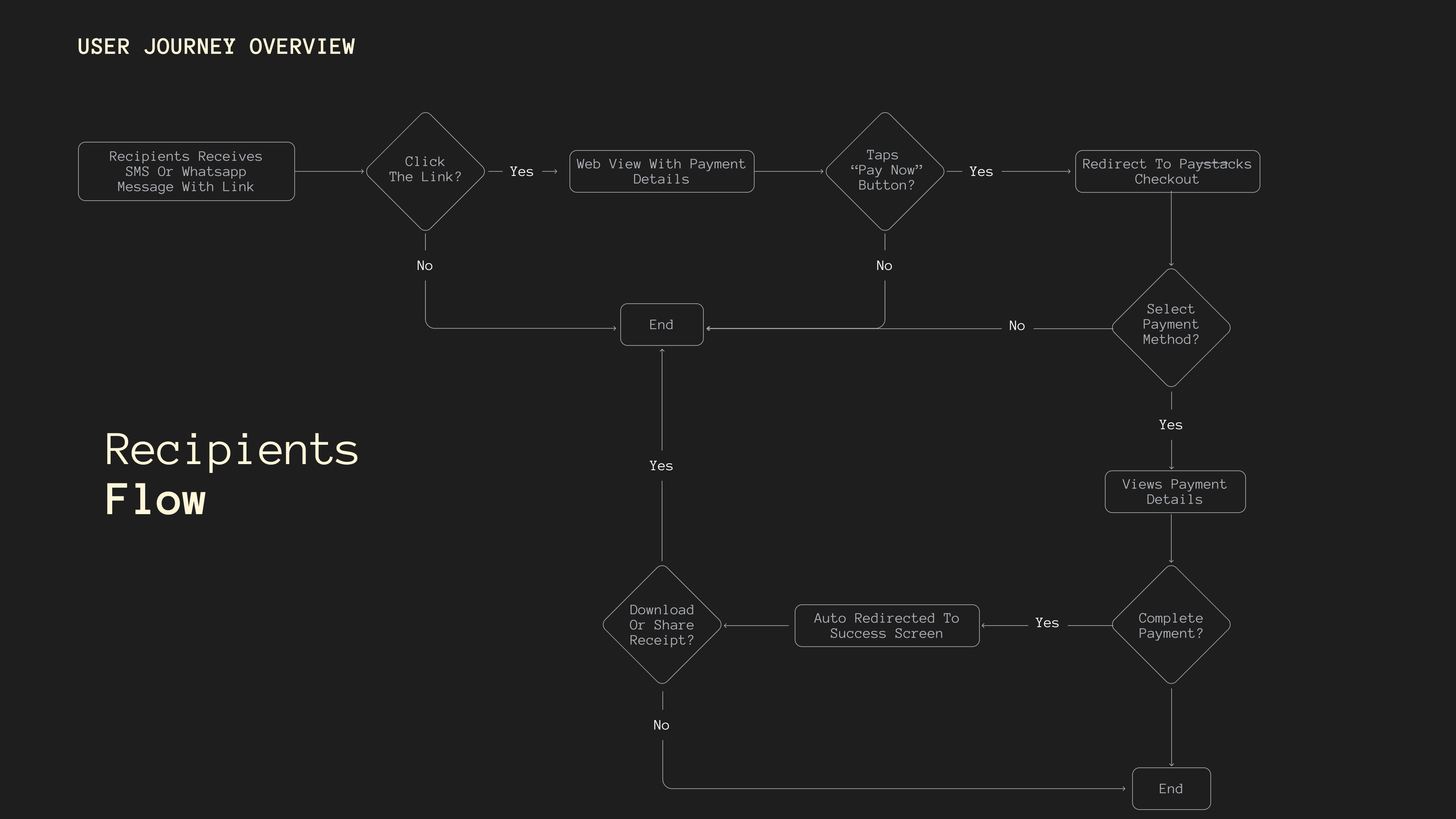

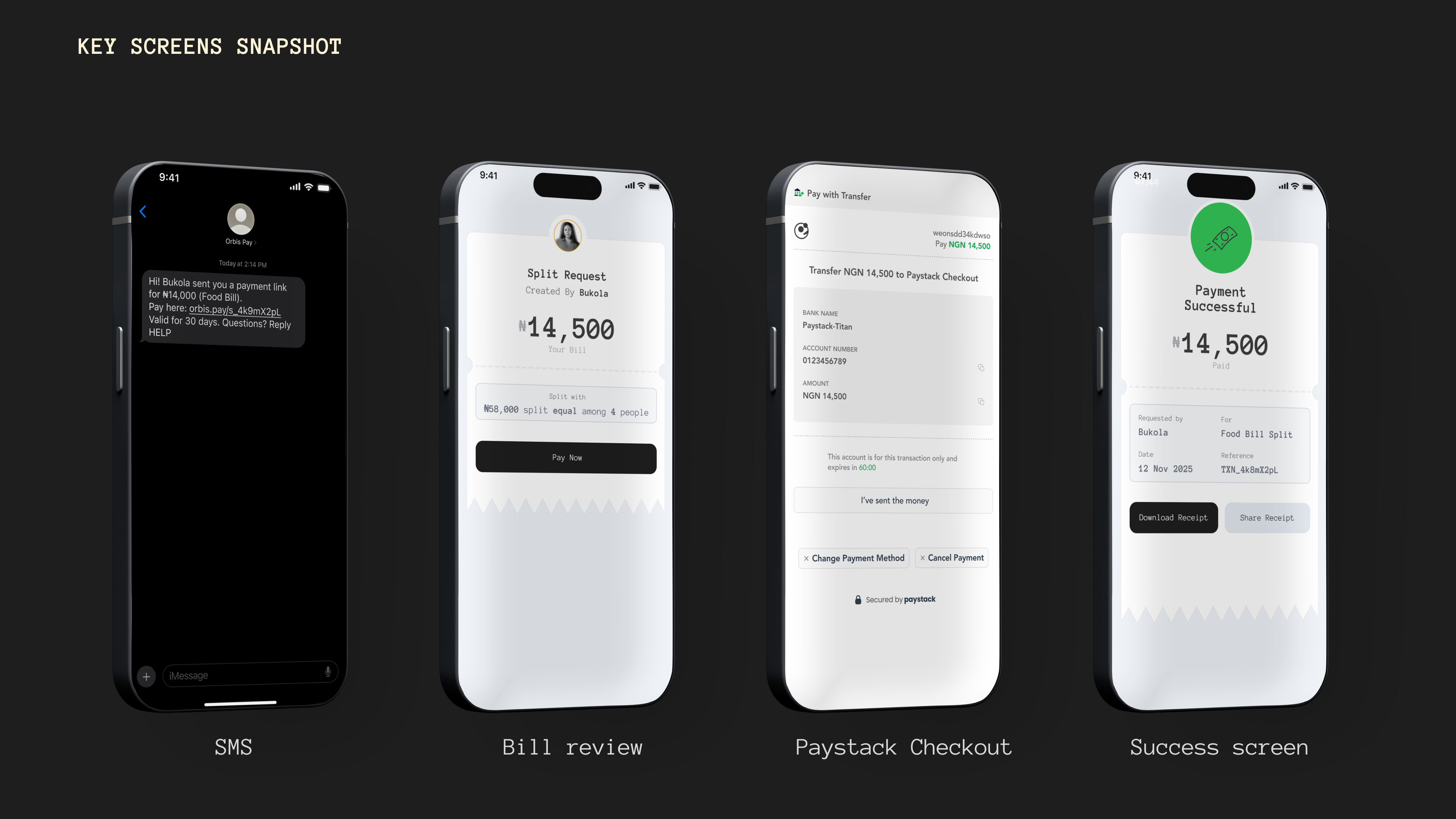

Decision 01 — Recipient-first, dual channels (SMS + WhatsApp). Requests reach people over WhatsApp and SMS — no install required to pay. The payer follows a link; the coordinator runs everything from the app. The reluctant payer is the bottleneck. Removing the install requirement removes the single biggest reason a debt stays unsettled.

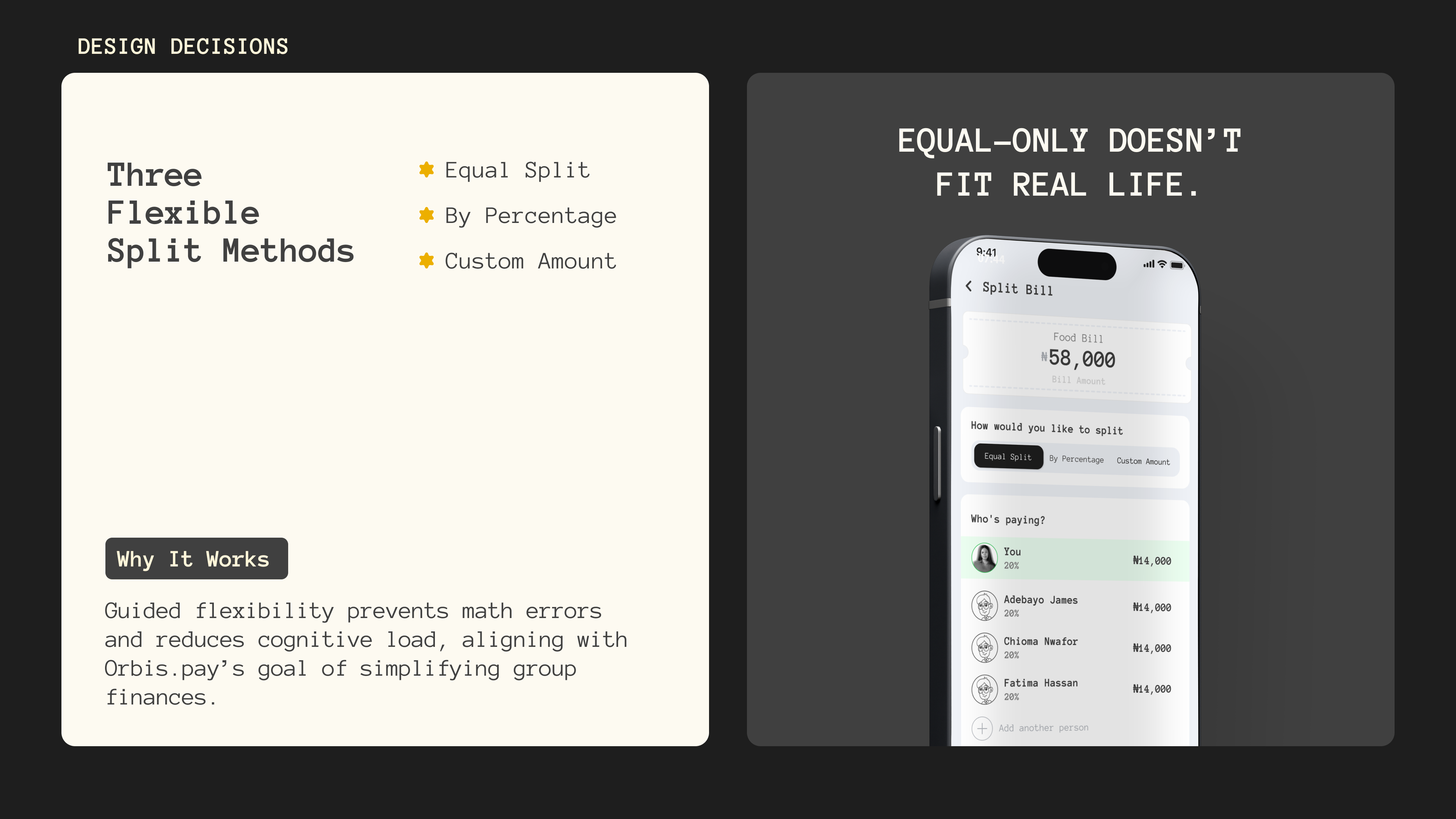

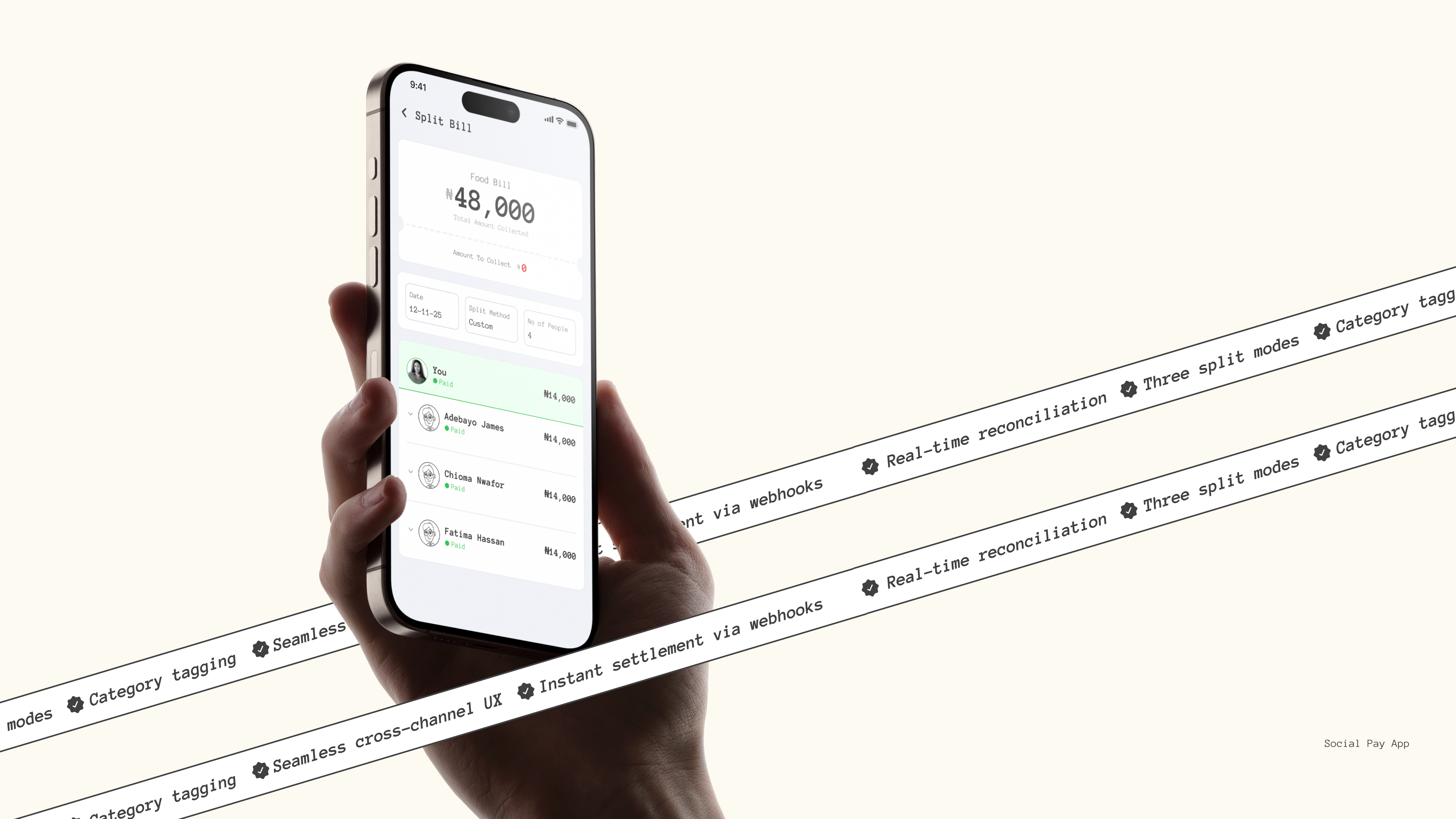

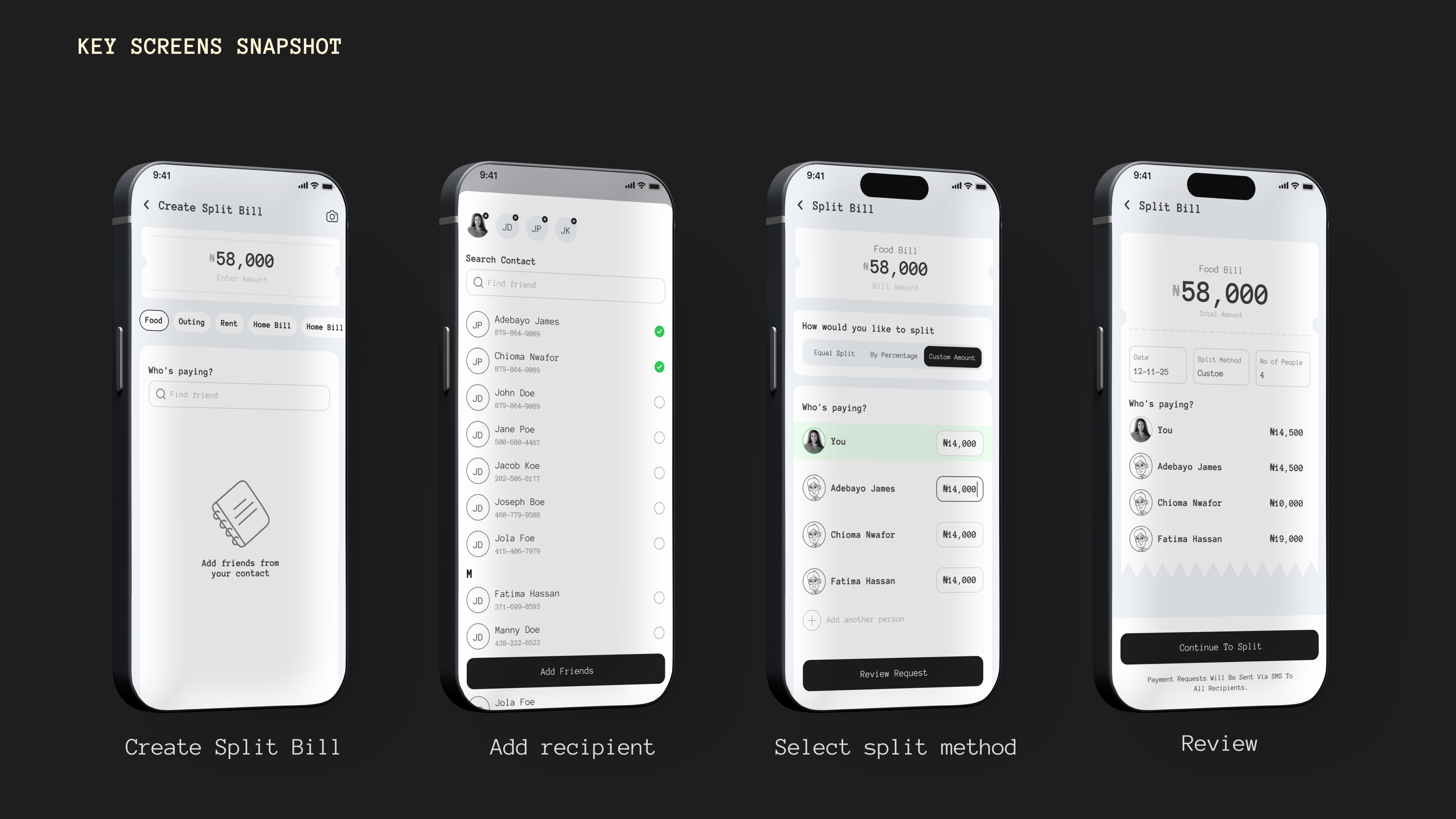

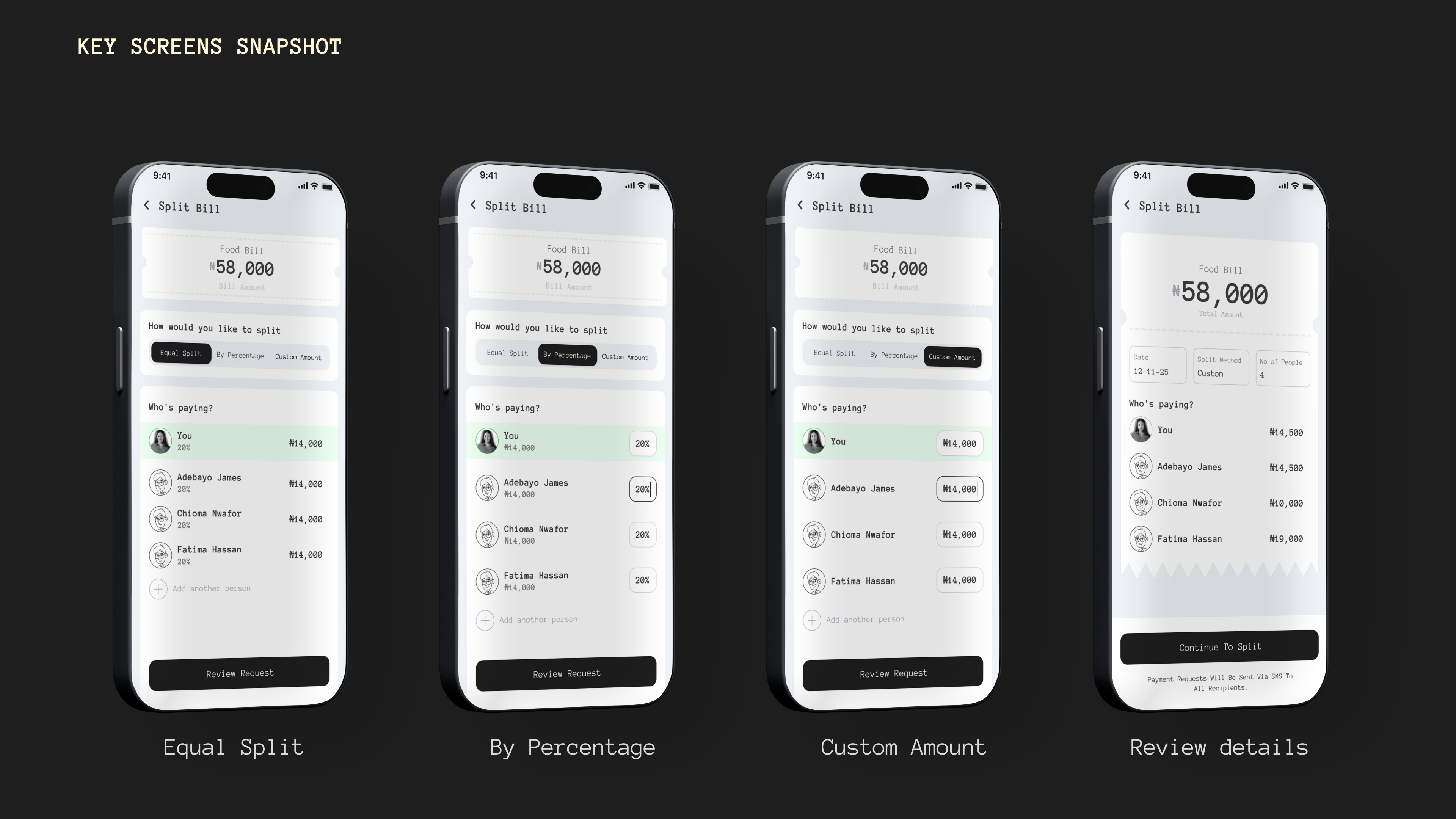

Decision 02 — Three flexible split methods.Even split, custom amounts, and by-item — surfaced in that order of expected frequency. Real bills aren't even. Forcing equal splits creates the exact off-platform negotiation the product is meant to absorb.

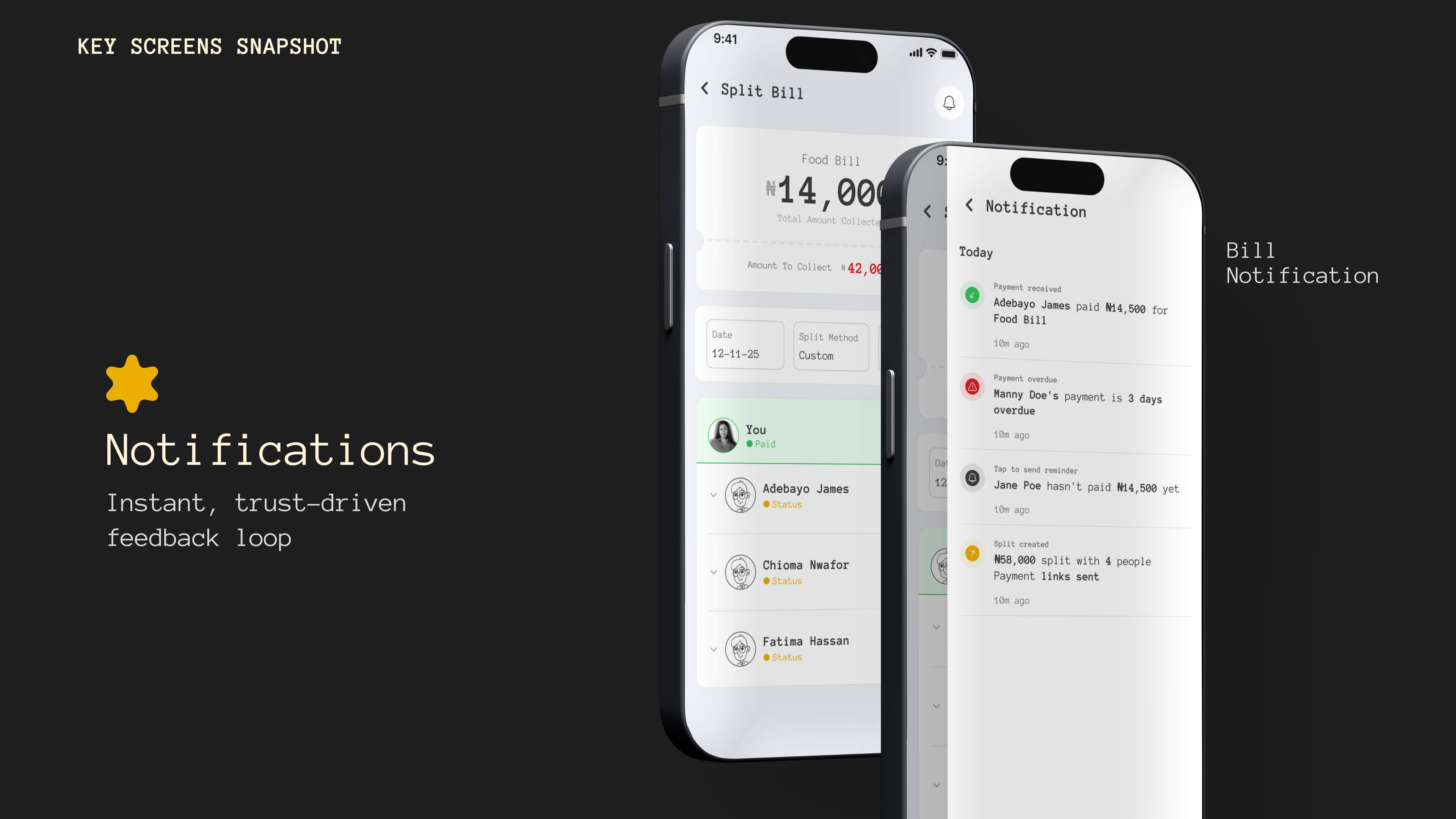

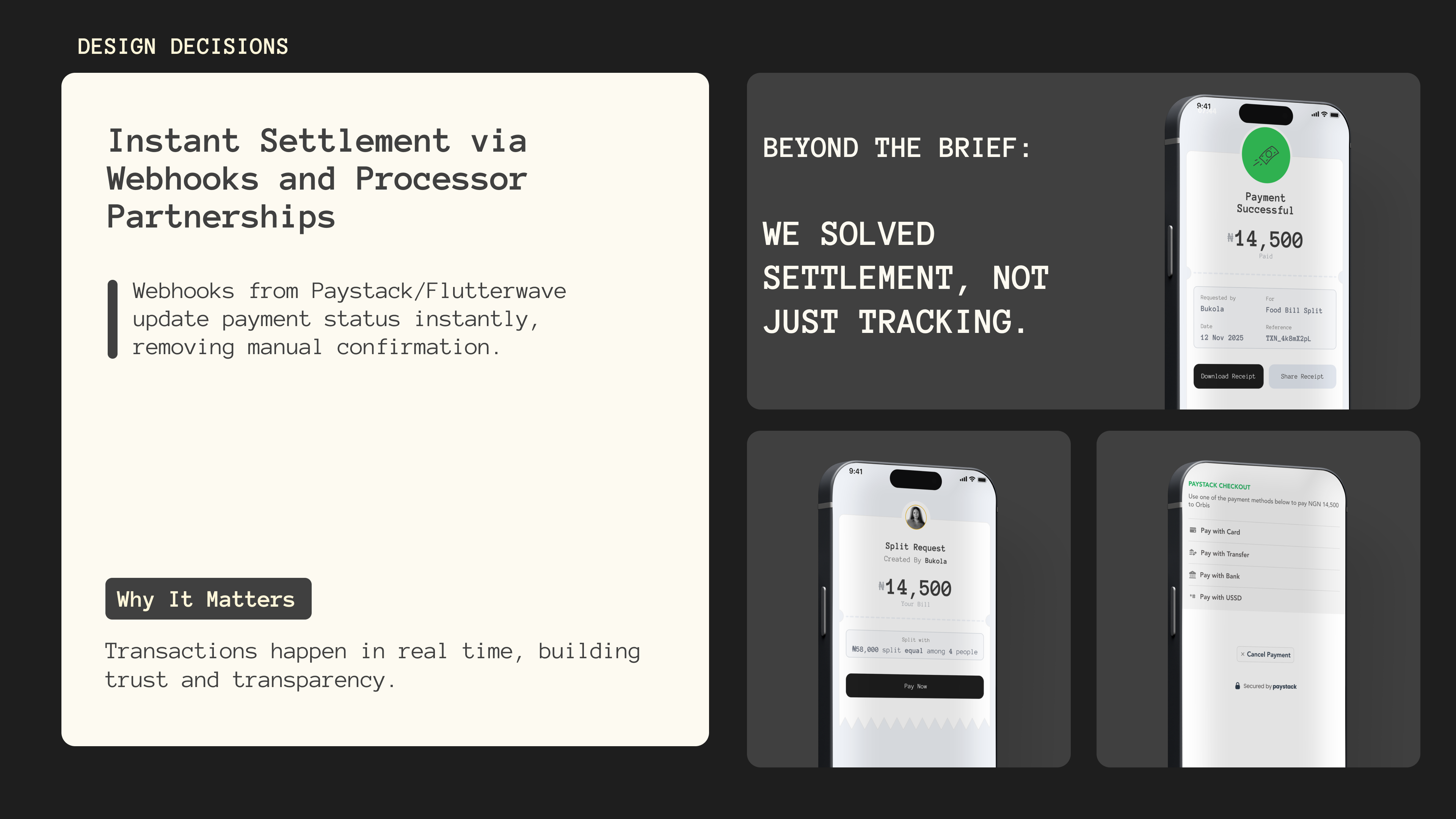

Decision 03 — Instant settlement via webhooks. Integrated with Paystack and Flutterwave so a payment updates status the moment it clears — no one has to vouch for anyone. Verified settlement is what makes the coordinator's dashboard true.

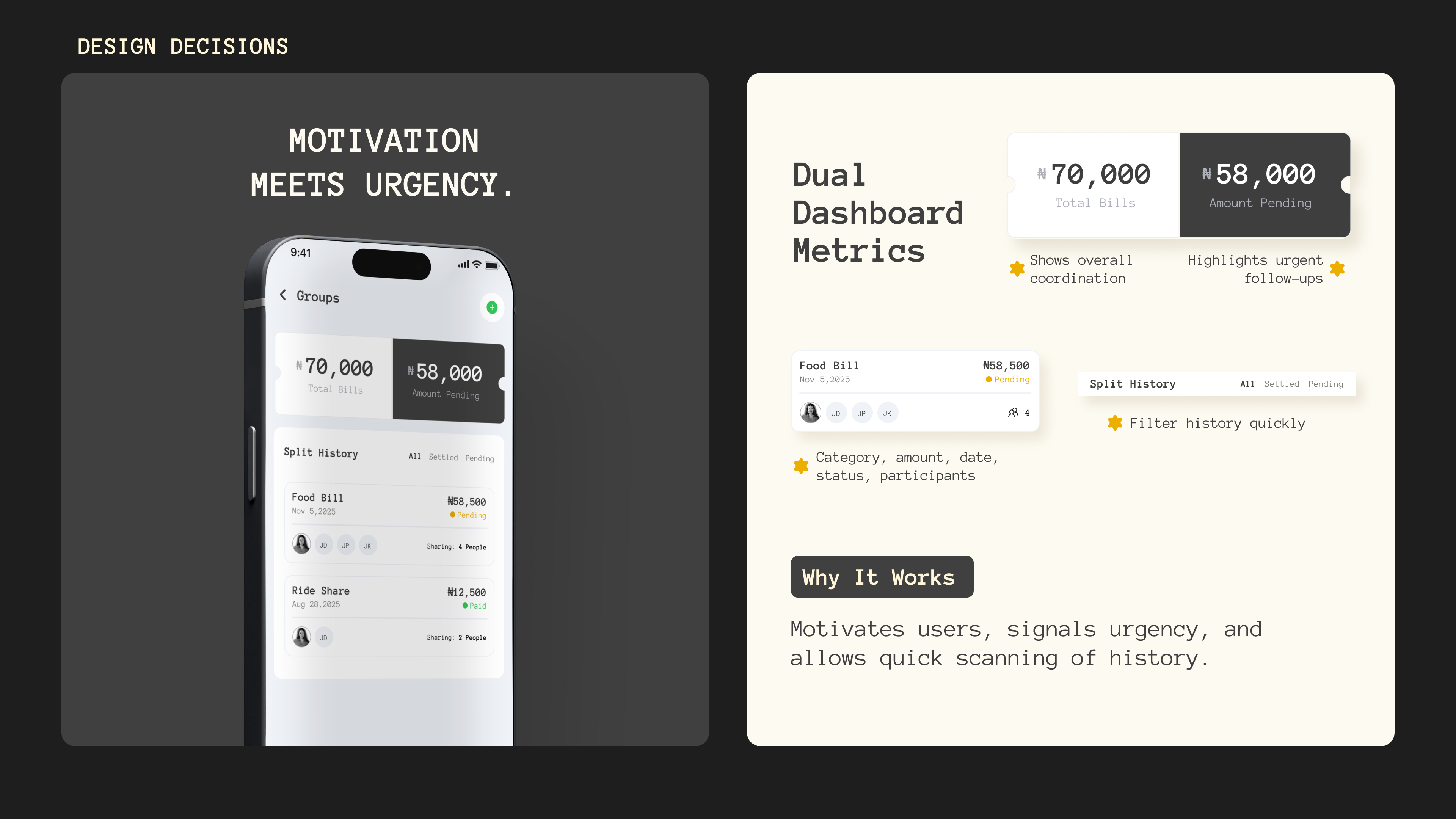

Decision 04 — A dashboard that measures settlement, not splits. The coordinator's dashboard leads with paid-versus-outstanding, not with the breakdown of the original bill. The split is history the moment it's sent. The only number that matters afterwards is how much is still owed.

Who it's for.

Bukola — the Coordinator. Always the one who fronts the bill and chases everyone after. Needs to know, at a glance, who has actually paid.

Chioma — the Pragmatist.Will pay, but won't tolerate friction. Needs the fewest possible steps from "I owe" to "done."

James — the Reluctant. Pays late, not out of malice but inertia. Needs a path so low-friction that ignoring it takes more effort than settling.

Requester & recipient flows.

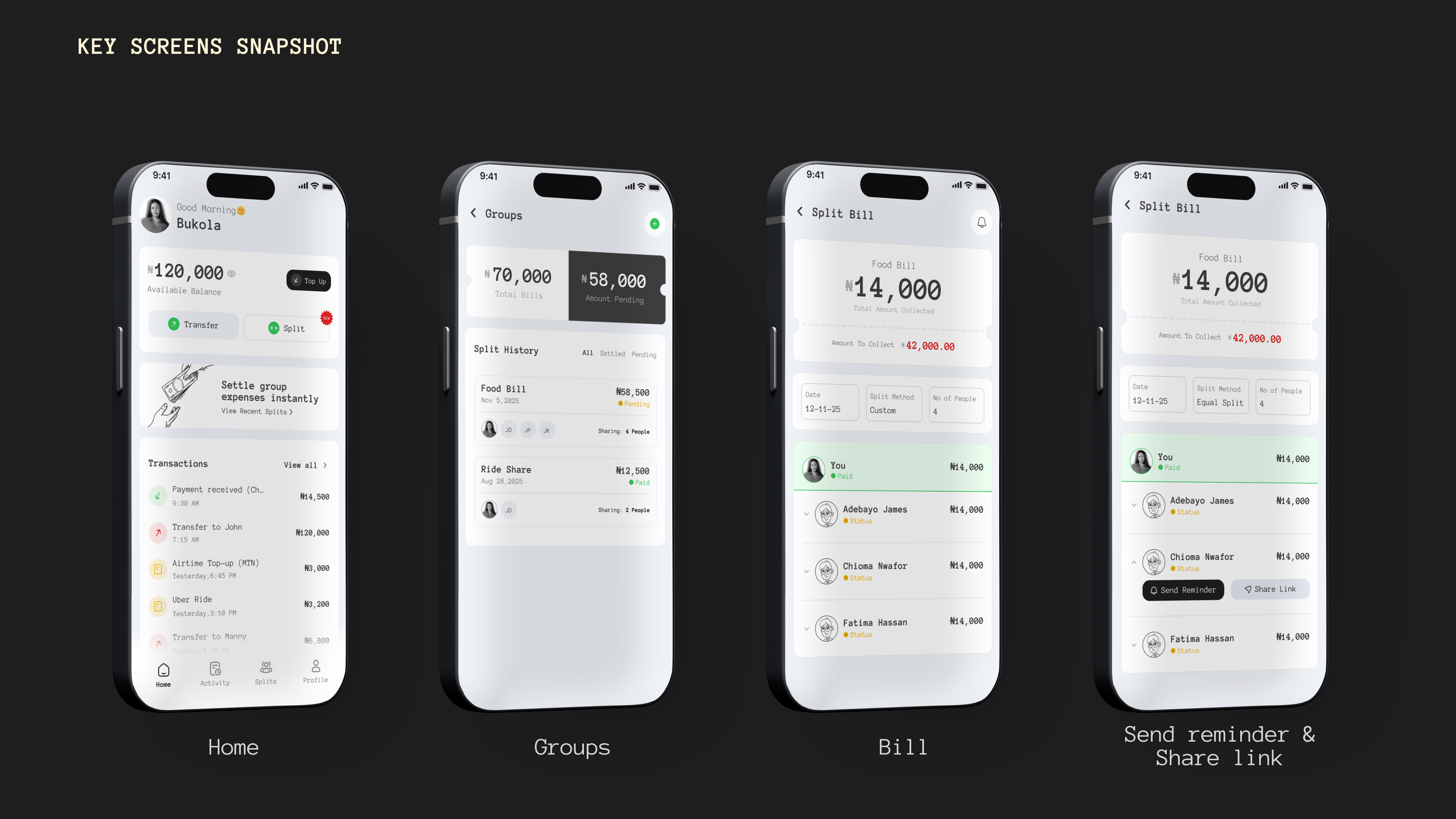

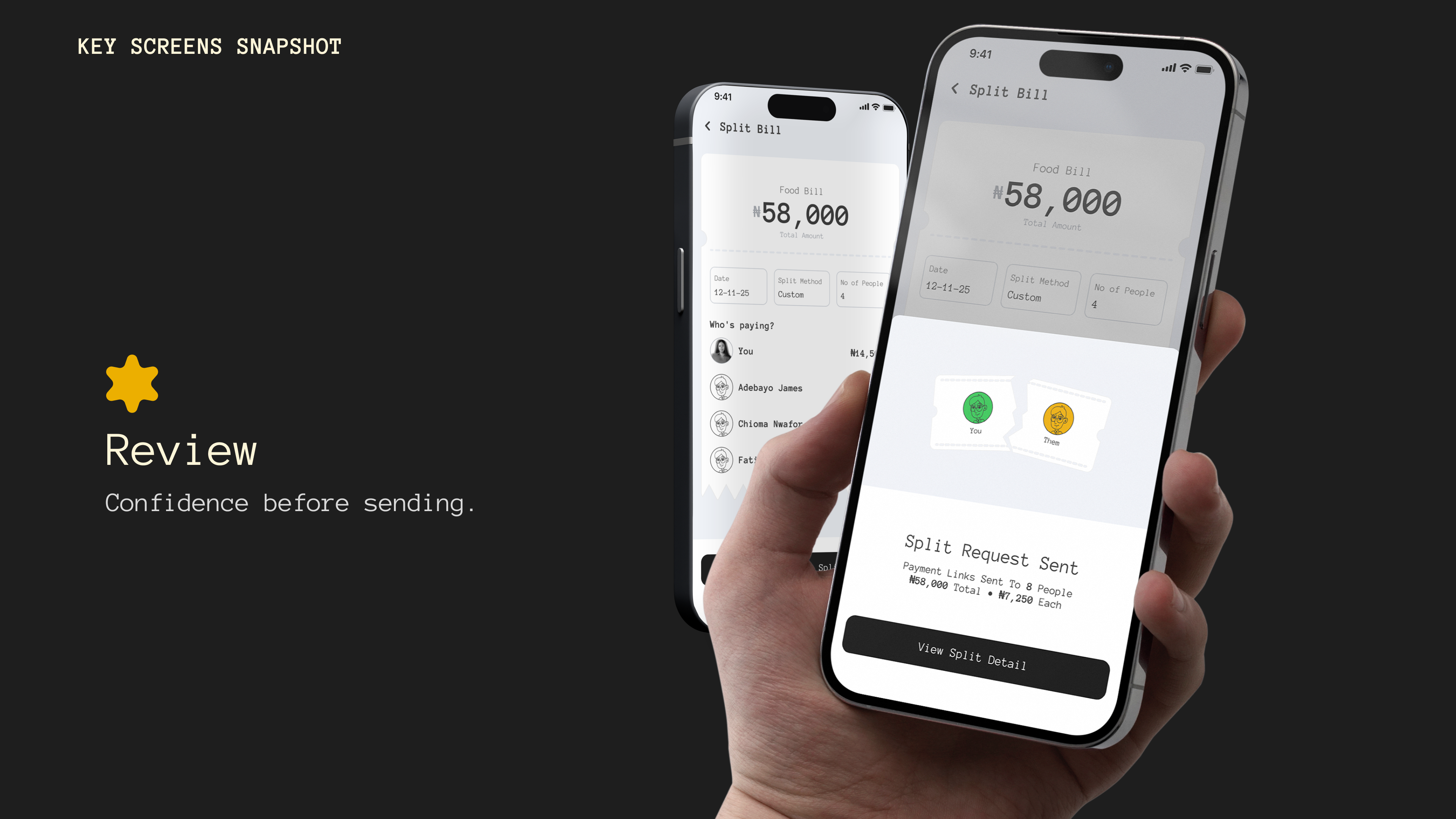

Home leads with Split alongside Transfer. Create Split Bill — amount, category tagging, recipients, split method — then review confirms the breakdown and sends payment links. The coordinator's dashboard leads with paid-versus-outstanding.

SMS or WhatsApp carries a branded message with the amount and a link. Bill Review is a lightweight web page — Pay Now, no account. Checkout handles card, transfer, bank, and USSD.

Orbis Split Bill is a strategy-led design, not a shipped product — so the honest outcome is the bet itself, not a metric. The bet: that the win here is converting an existing off-platform habit, not manufacturing a new one.

The opportunity is real and already in motion — a large, chat-native audience splitting money by hand inside WhatsApp every day, on payment rails that already clear in seconds. The design's whole job, when built, is to sit inside that behaviour and remove the single step that breaks it: settlement.

When 140M people are already splitting money in chats, design should listen first.